A company's board of directors needs to verify that the organization's compliance program is actually effective, rather than just a "paper program." What is the most effective approach for the board to fulfill this oversight responsibility?

Select an answer to reveal the explanation.

Short Explanation and Infographic

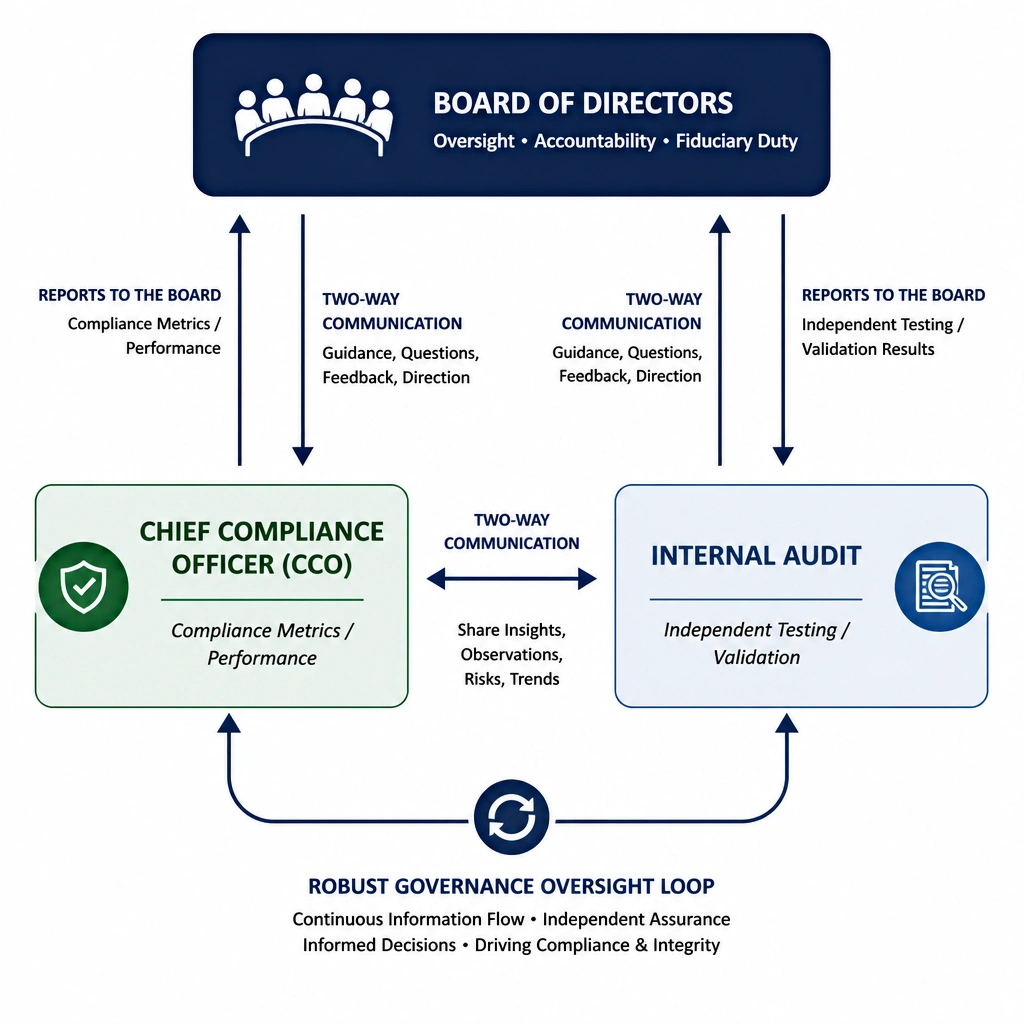

Here’s the deal: a board of directors can't just set up a compliance program, walk away, and hope for the best. That’s a classic recipe for disaster. They have a fiduciary duty to make sure the program actually works! But they also can't micro-manage every single detail. If you look at option B, this is where the magic happens. By sitting down regularly with both the Chief Compliance Officer and Internal Audit, the board gets a direct, unfiltered look at what’s really going on—the real-world risks and how they are being handled. They aren't getting bogged down in minor details like who forgot to sign a training log, but they are getting the big-picture oversight they need. Trust me on this, regular communication with your key compliance leaders is what separates a world-class program from a check-the-box paper shield. Got it? Sweet. Let's keep rolling!

Full explanation below image

Full Explanation

The correct answer is B. Fiduciary and regulatory expectations (such as those outlined in the U.S. Sentencing Guidelines and DOJ compliance guidance) require the board of directors to exercise reasonable oversight regarding the implementation and effectiveness of the compliance program. The most effective way to achieve this is through regular, meaningful engagement with the Chief Compliance Officer (CCO) and the Internal Audit function. These discussions allow the board to assess risk metrics, program resources, audit results, and management’s responsiveness to compliance issues.

Option A is incorrect because requiring the CCO to attend all business and sales meetings is operationally impractical, inefficient, and blurs the line between management and oversight. It would dilute the compliance officer's strategic focus. Option C is incorrect because replacing the compliance manager annually destroys program continuity, prevents the development of deep institutional knowledge, and disrupts relationships built on trust between compliance and business units. Option D is incorrect because reviewing every minor infraction drowns the board in operational noise and administrative trivia, preventing them from focusing on high-level systemic risks, governance, and strategic program performance.