An internal compliance audit reveals that a company's controls for approving large third-party payments are severely deficient. What should be the compliance department's primary course of action in response to this finding?

Select an answer to reveal the explanation.

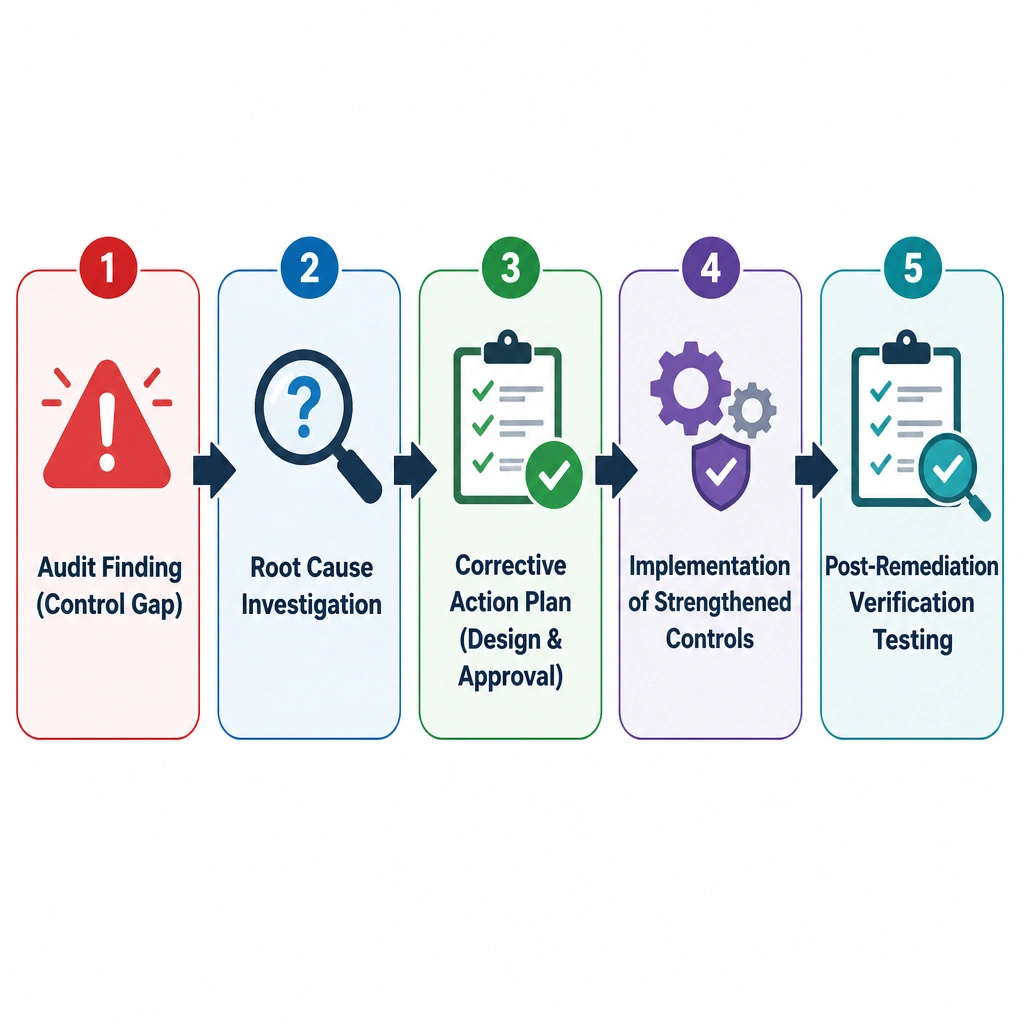

Short Explanation and Infographic

Imagine you're doing a routine check of your house's security system and you find out the back door lock doesn't work. What do you do? You don't ignore it (Option A) and hope burglars don't notice, and you definitely don't fire the guy who told you about it (Option B)! You go fix the lock immediately. That's what a corrective action plan is all about. When an audit reveals a weak link in your payment controls, that's a massive red flag. If you don't plug that gap, you're practically inviting fraud or bribery to slip through. The correct answer is D. You have to step up, put a corrective plan in place, and reinforce those controls. Publicly announcing it before you even know what went wrong (Option C) is just bad crisis management. Fix the lock first!

Full explanation below image

Full Explanation

The correct answer is D. When a significant control deficiency or compliance vulnerability is identified through an internal audit, the organization must act swiftly to remediate the issue. Regulatory bodies, such as the US Department of Justice (DOJ), place substantial weight on an organization's response to detected weaknesses. Failing to act on internal audit findings indicates a systemic compliance failure and can significantly increase legal liability if a regulatory violation occurs due to the unaddressed gap. A corrective action plan should outline specific remediation steps, assign owners, set deadlines, and establish follow-up testing to verify that the control gap has been successfully closed.

Let's evaluate the incorrect options: - Option A is incorrect because ignoring audit findings exposes the company to severe legal, financial, and regulatory risks, especially in third-party payments which are a primary vector for bribery and corruption. - Option B is incorrect because penalizing or redirecting the audit team undermines the independence of the internal audit function, creating a culture of fear and suppressing future reporting of critical risks. - Option C is incorrect because while public disclosure might eventually be legally required (such as in public filings for material weaknesses), doing so immediately without a remediation plan or investigation is premature and commercially damaging.

By establishing a robust corrective action plan, the compliance team demonstrates to the board and regulators that the organization has a functioning detective control and is committed to continuous improvement and risk reduction.