An organization structures its sales compensation plan to reward bonuses and commissions based solely on gross revenue, with no connection to compliance standards or internal policies. What primary risk does this incentive model introduce?

Select an answer to reveal the explanation.

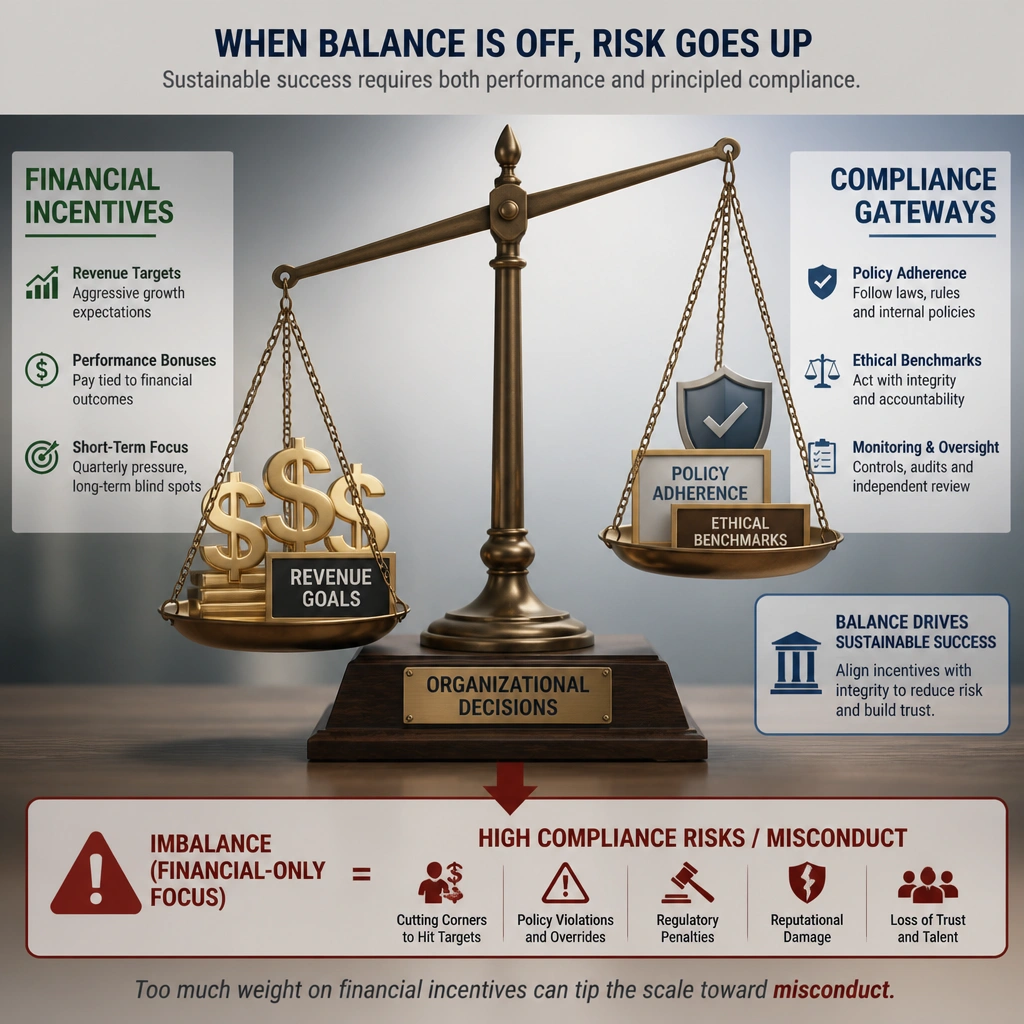

Short Explanation and Infographic

Think of it like this: if you tell a greyhound that it only gets fed if it catches the rabbit, that dog is going to run through brick walls, jump fences, and bite anything in its way to get that food. When you pay your sales team only on revenue, without checking how they got that revenue, you're setting up a compliance time bomb. Sales reps will start taking shortcuts. They might pay a kickback, bribe a foreign official, or falsify contracts just to hit their numbers and get paid. The correct answer is A. You've got to align incentives with your values. If you reward bad behavior, you're going to get bad behavior. Options B, C, and D miss the mark because revenue-only plans actually motivate people—they just motivate them to do the wrong things! Keep your incentives balanced with compliance checkpoints.

Full explanation below image

Full Explanation

The correct answer is A. Incentive structures are powerful drivers of corporate culture and behavior. When compensation, bonuses, or commissions are tied exclusively to financial metrics (like gross revenue or sales volume) without accounting for compliance, ethics, or internal policies, it creates a perverse incentive. Employees may feel pressure to close deals at any cost, leading to high-risk behaviors such as offering bribes (violating the FCPA), engaging in collusive pricing, falsifying sales records (channel stuffing), or ignoring customer due diligence requirements. Regulatory bodies, such as the DOJ, specifically evaluate whether a company's compensation structures incentivize ethical behavior and penalize compliance failures.

Let's examine why the other options are incorrect: - Option B is incorrect because revenue-only incentives typically increase short-term motivation and sales drive, though they direct it in a way that ignores compliance and ethics. - Option C is incorrect because incentive structures do not dictate the physical size of the sales team, which is a staffing and capacity decision made by sales management and HR. - Option D is incorrect because while compliance failures may increase training needs later, administrative training expenditures are not the primary compliance risk of a revenue-only compensation structure.

To mitigate these risks, modern compliance programs implement clawback provisions, include compliance metrics in performance reviews, and tie incentive payouts to both commercial success and adherence to company policies.