A multinational organization is expanding its sales operations into a jurisdiction identified by the Financial Action Task Force (FATF) as having a high risk for money laundering. Which of the following preventive controls is most critical for the compliance team to establish in this region?

Select an answer to reveal the explanation.

Short Explanation and Infographic

Check this out. When you're operating in high-risk zones, you can't just close your eyes and hope for the best. And you definitely can't let customers pay with briefcases of cash without asking questions! That's a one-way ticket to a federal investigation. At the same time, shutting down all business in that country might not be realistic either. The sweet spot here is implementing a rock-solid 'Know Your Customer'—or KYC—program, along with transaction tracking. You need to know exactly who you're dealing with and monitor where the money is flowing. Trust me, having these controls in place is your best defense. C is the only way to go.

Full explanation below image

Full Explanation

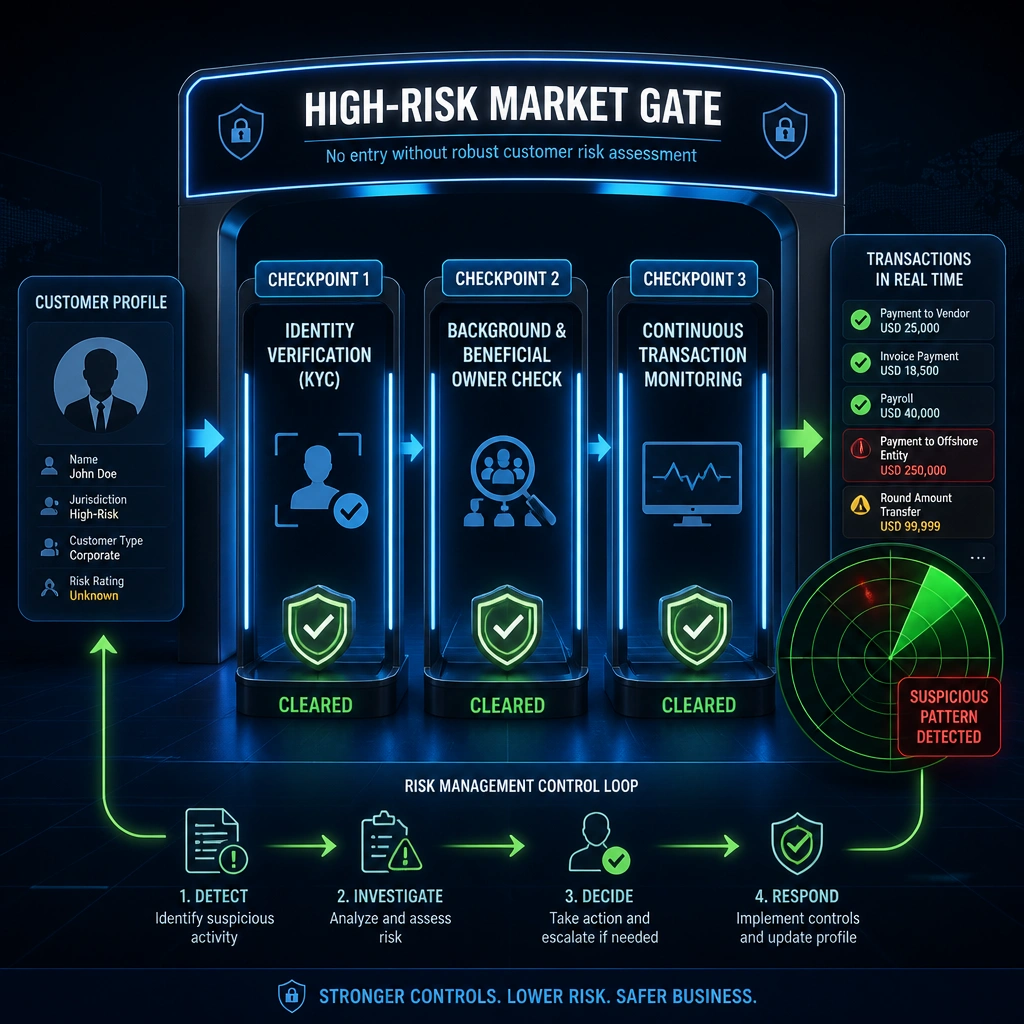

Operating in high-risk jurisdictions for money laundering requires a robust and structured Anti-Money Laundering (AML) compliance framework. The foundation of such a framework is the implementation of a comprehensive 'Know Your Customer' (KYC) program alongside continuous transaction monitoring. KYC procedures require the organization to verify the identity of its clients, determine the beneficial ownership of corporate entities, and assess the risk profile of each business relationship before transaction processing begins. Transaction monitoring ensures that subsequent financial activities align with the client's known business profile, allowing the compliance team to detect and report suspicious patterns, such as structured transactions or unexplained third-party payments.

Let's examine why the alternative choices are incorrect: - Option A represents 'de-risking,' which is an extreme operational decision rather than a compliance risk management control. While organizations must assess risk tolerance, blanket bans on entire countries are often commercially unfeasible and do not address how to safely manage remaining risk. - Option B is incorrect because unrestricted cash transactions are one of the primary vectors for laundering illicit funds. Allowing cash without due diligence violates basic AML regulations. - Option D is incorrect because consolidating financial authority in a single individual violates the core principle of segregation of duties. This creates a severe internal control vulnerability, increasing the likelihood of collusion, fraud, or unmonitored illicit payments.

By enforcing KYC and transaction tracking (Option C), the company can actively manage risk, maintain regulatory compliance, and protect itself from being used as a conduit for financial crimes.