An organization's internal audit scope is restricted exclusively to testing financial and accounting controls. From a compliance and ethics perspective, what is the primary weakness of this audit strategy?

Select an answer to reveal the explanation.

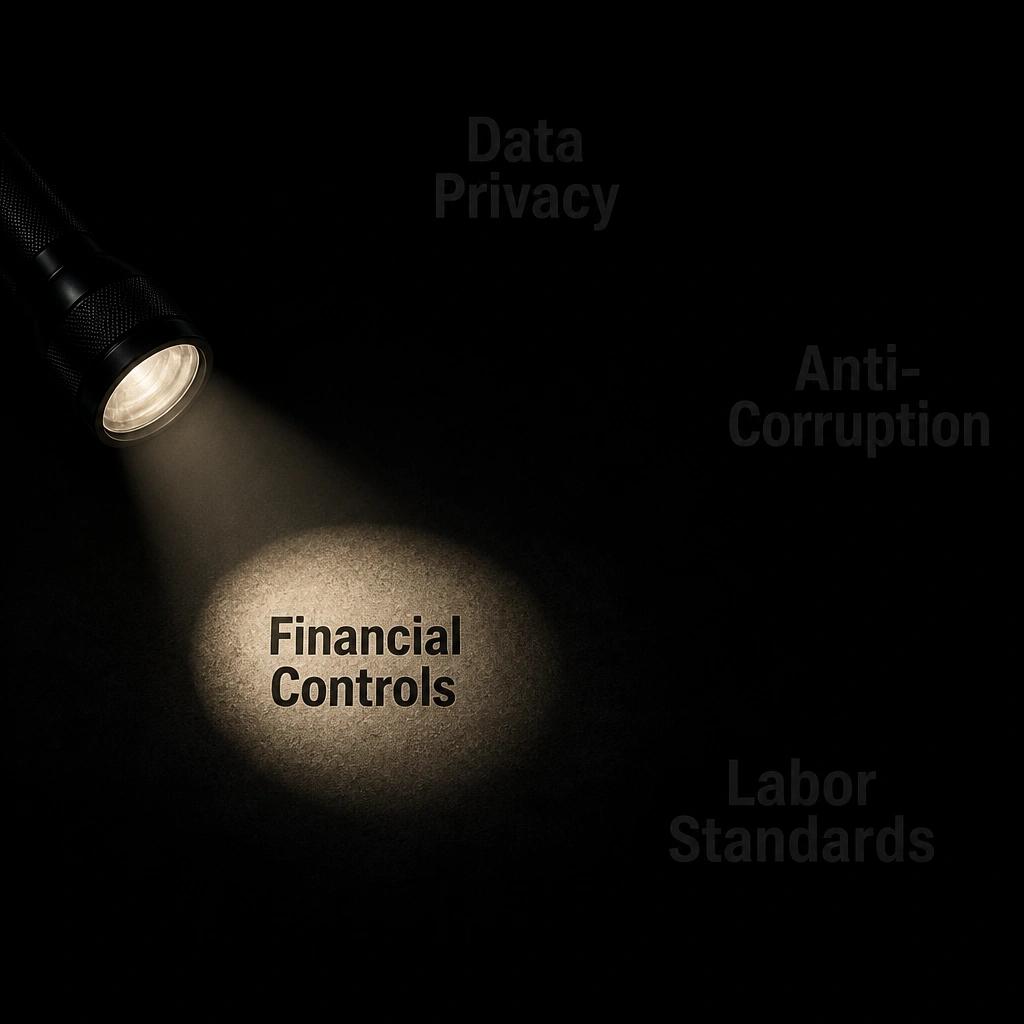

Short Explanation and Infographic

Check this out: a lot of companies think that if their financial audits are clean, their compliance program must be in great shape. But that is a huge trap! Financial controls are designed to make sure the math adds up and nobody is stealing from the cash drawer. They are not designed to catch non-financial violations like bribery, environmental violations, or data privacy breaches. If your internal audit program only looks at financial controls, you are leaving a massive blind spot. You could have a perfectly balanced ledger while your sales team is bribing foreign officials to win contracts. That's why your audit strategy needs to cover both financial and non-financial compliance risks. If you only look at the numbers, you're missing the real dangers. Trust me on this!

Full explanation below image

Full Explanation

An effective compliance program must feature an audit plan that covers all high-risk areas of the business. While financial audits ensure the integrity of financial statements and detect financial statement fraud, they do not assess compliance with operational, environmental, or social regulations. A strategy that focuses solely on financial controls creates a major compliance vulnerability. Significant non-financial risks, including Foreign Corrupt Practices Act (FCPA) behavioral violations, General Data Protection Regulation (GDPR) breaches, and environmental or labor law infractions, will go unchecked because standard financial audits do not monitor these areas. Let's analyze the incorrect choices: - Option B is incorrect because limiting the scope to financial controls actually simplifies the audit process, though it exposes the company to unmitigated risk. - Option C is incorrect because a financial-focused audit is designed specifically to meet external financial standards (e.g., Sarbanes-Oxley Act compliance) and is highly effective for that purpose; its weakness is its failure to address broader compliance and ethics risks. - Option D is incorrect because restricting the scope to financial auditing typically lowers the cost by avoiding the need to hire specialized operational or compliance auditors. To ensure comprehensive risk mitigation, internal audit plans must coordinate with the compliance department to audit controls across both financial and non-financial risk areas.