An engineering team is evaluating two machine learning regression models for forecasting equipment failure. They use Mean Squared Error (MSE) as their primary accuracy metric. Model X yields an MSE of 0.012, while Model Y yields an MSE of 0.035. Assuming other factors such as resource requirements are comparable, which model should be selected and why?

Select an answer to reveal the explanation.

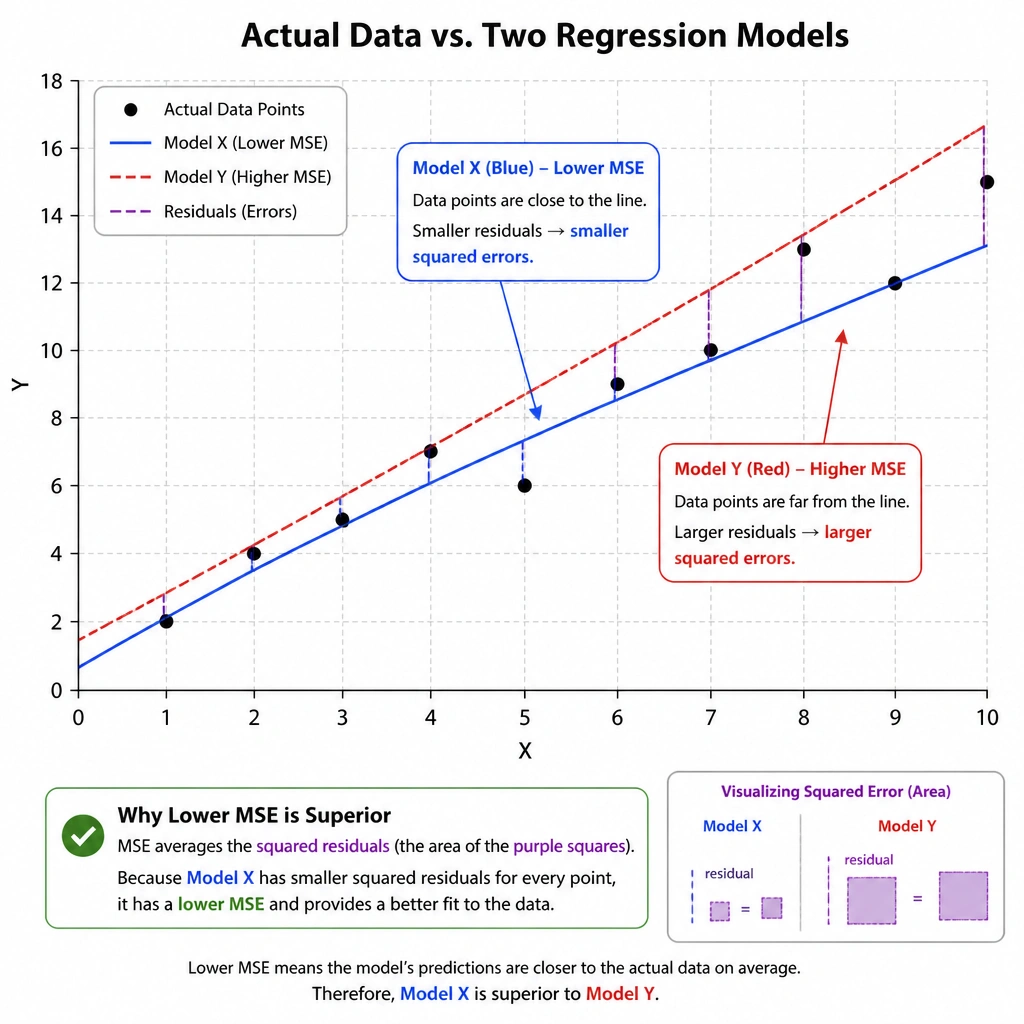

Short Explanation and Infographic

Okay, let's keep it simple. Mean Squared Error (MSE) measures the average of the squares of the errors—that is, the difference between what your model predicts and what actually happens. So, is a big error good or bad? It's bad, obviously! You want your errors to be as close to zero as possible. That means a lower MSE is always better. Model X has an MSE of 0.012, and Model Y has an MSE of 0.035. Model X has a much lower error, meaning its predictions are far more accurate. Don't fall for the trick options that claim high error means better generalization or complexity. On the test and in the real world, you want accuracy, and a lower MSE gives you exactly that.

Full explanation below image

Full Explanation

Mean Squared Error (MSE) is a standard metric used to evaluate regression models by calculating the average squared difference between estimated values and actual values. The mathematical formula squaring the residuals penalizes larger errors more heavily. Because MSE represents error, a smaller value indicates that the model's predictions are closer to the true data points, representing superior predictive performance. Therefore, Model X (MSE of 0.012) is preferred over Model Y (MSE of 0.035) because it minimizes the error rate. Distractors that suggest higher MSE prevents overfitting or indicates complexity are conceptually incorrect; a higher error rate simply represents lower accuracy on the evaluated dataset. Additionally, MSE scores alone do not reflect the interpretability or internal complexity of a model's architecture.