A multinational firm wants to evaluate the operational effectiveness of its local compliance controls without immediately resorting to a full-scale external audit. The compliance officer instructs department heads to conduct a Control Self-Assessment (CSA). What is the primary purpose of this exercise?

Select an answer to reveal the explanation.

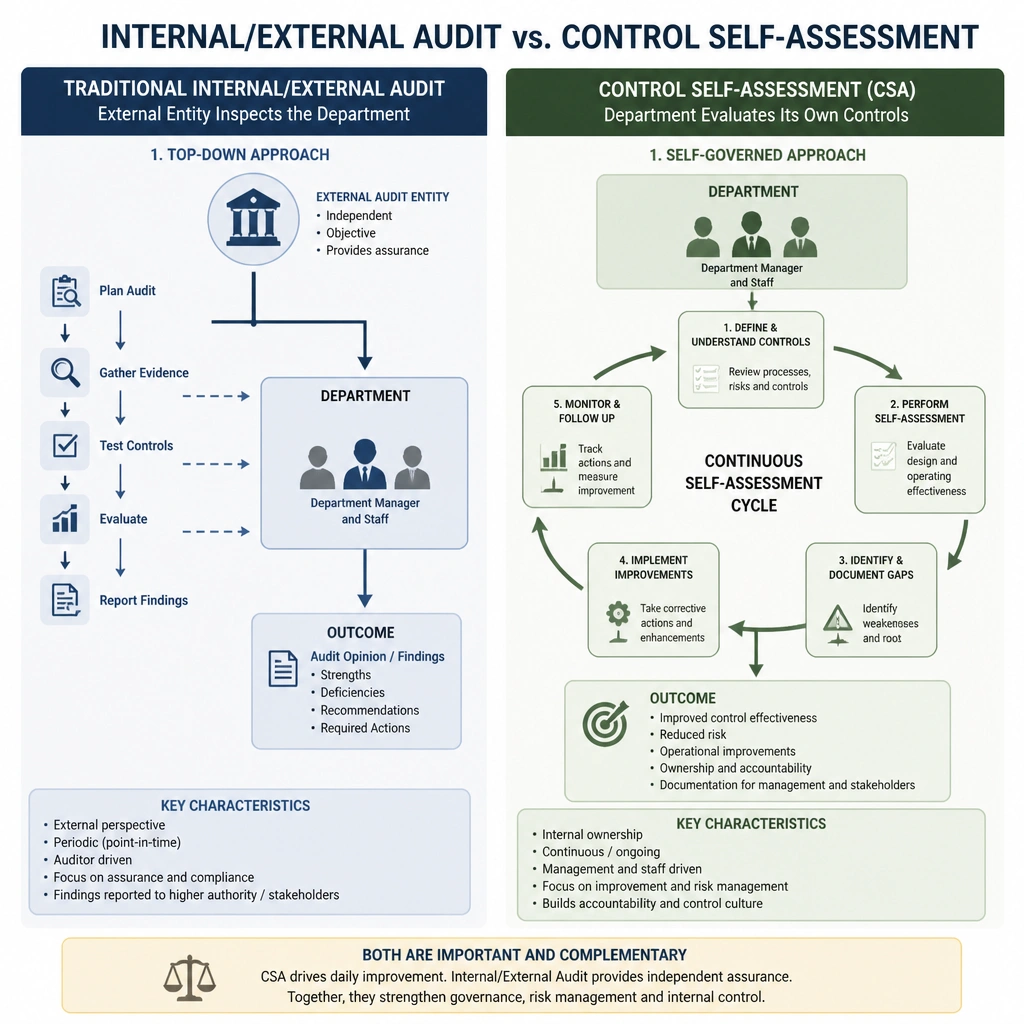

Short Explanation and Infographic

Check this out: a Control Self-Assessment, or CSA, is exactly what it sounds like. Instead of waiting for the internal audit team to come in with their clipboards and point out your flaws, the managers of the business units evaluate their own controls. It's like doing a self-diagnostic on your own car before taking it to the mechanic. The cool thing is, it gets local managers to take ownership of their own compliance environment. Got it? Sweet.

Full explanation below image

Full Explanation

A Control Self-Assessment (CSA) is a management technique where business unit managers and their teams directly evaluate the adequacy and effectiveness of the internal controls within their own departments. Unlike external or independent internal audits, which are performed by objective third parties, a CSA relies on the people closest to the processes to identify control gaps, assess risks, and implement corrective actions. This approach promotes a stronger compliance culture by fostering accountability and ownership of risk management at the operational level. CSAs do not replace independent auditing, but they serve as a powerful first line of defense. They are not used to assess employee satisfaction (which is HR-driven), nor are they external financial audits (which require independent CPAs). While they may indirectly improve operational efficiency, their primary objective is control verification, not commercial business performance metrics.