A multinational enterprise is onboarding a new distributor in a region known for high corruption risk. Why must the compliance team perform a structured third-party risk assessment prior to finalizing the agreement?

Select an answer to reveal the explanation.

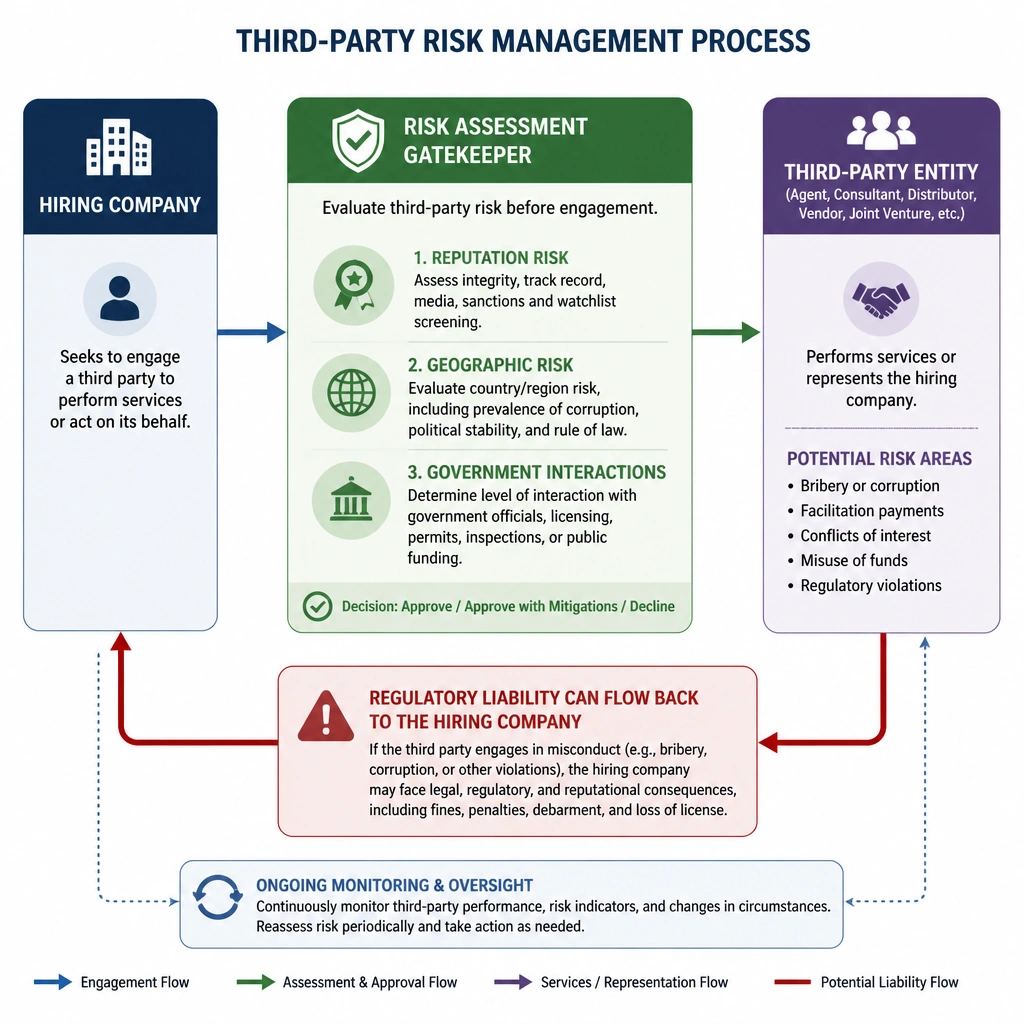

Short Explanation and Infographic

Check this out: when you hire a third party—whether they're a distributor, an agent, or a supplier—you don't just inherit their help, you inherit their compliance headache too! In the real world, if a third-party partner hands out a bribe to get a deal done on your behalf, guess who the regulators are going to visit? Yep, your company. You can't just stick your head in the sand and pretend you didn't know. That's why we run third-party risk assessments. It's all about figuring out the risk that their actions might drag your company into a regulatory nightmare. Trust me on this, failing to do due diligence here is one of the quickest ways to end up in the news. You want to spot the red flags before you sign on the dotted line, not when the boss walks in with a subpoena!

Full explanation below image

Full Explanation

The primary objective of a third-party risk assessment is to evaluate the risk that a third-party partner's actions could lead to a compliance violation or legal liability for the hiring organization. Under international anti-corruption frameworks, such as the U.S. Foreign Corrupt Practices Act (FCPA) and the UK Bribery Act, organizations can be held criminally liable for corrupt activities conducted by third parties acting on their behalf. Consequently, robust due diligence and risk assessments are essential preventative controls to identify potential compliance gaps, corruption risks, or ethical concerns before establishing a business relationship. Option A is incorrect because cost negotiation is a procurement and finance function, not the primary objective of a compliance risk assessment. Option B is incorrect because aligning payroll software is an IT or accounting integration concern, unrelated to identifying compliance risks. Option C is the correct answer because it directly addresses the mitigation of regulatory liability stemming from third-party conduct. Option D is incorrect because employee attendance and marketing campaigns are operational metrics that do not address the core compliance risk of third-party violations.